Greetings,

The festival season has started and there is happiness, excitement, and energy all around. You find immense satisfaction in seeing the contentment on your loved ones’ faces as this is what you have been slogging for day-in, day out. You love to spend time with them and cherish these memories for a lifetime.

With you being the breadwinner, your family has little to worry about when it comes to their financial expenses.

The sad reality, we all are unaware of what the future holds. Lots of people die prematurely every year either by way of illness, accident, etc.

And if you happen to be the only breadwinner for your family and you were to pass away, it could lead to devastating consequences for your loved ones.

Your absence could lead to their inability to manage household expenses, pay debt and maintain the standard of living leading to financial hardship for your loved ones.

==============================================================================

Can you and your family survive if your monthly income decreases by 30%?

The answer is probably no. A 30% decrease in income can be a major financial hardship, and it can be difficult to make ends meet.

If 30% can play such havoc, how about 100% income stopping? This scenario is a definite possibility if the breadwinner of the family dies.

The family would lose their entire source of income. They would have to find a way to pay for their housing, food, transportation, and other expenses on their own. This can be a daunting task, and it is not something that everyone is prepared for.

This is why it is so important to have life insurance. Life insurance provides financial security for your family in the event of your death. It helps them to pay for their expenses and maintain their standard of living.

Life insurance is not just for the wealthy. It is a basic need for every family. If you have dependents, you should have life insurance. It is the best way to protect your family’s financial future.

Life Insurance is necessary. It is essential. It is a must-have for every family.

==============================================================================

The least you can do, therefore, is to secure your family’s financial future by buying a life insurance policy. When you get Life Insurance, you are buying a DEATH BENEFIT!

This benefit will be paid to your nominee (wife/children/nominee) in case of your untimely death.

With the purchase of Life Insurance, your family’s future is secure as they now have a FINANCIAL SAFETY NET that continues even in your absence.

Thus, ensuring that even in your absence, being the sole breadwinner, your loved ones will not have to go through financial hardship.

True they will have to face the harsh emotional reality of you not being there but at least their financial dreams are protected and they can continue to have quality education and maintain the current standard of living.

Life Insurance will help your family get a sense of stability and comfort during what would undoubtedly be an emotionally challenging time in spite of your absence.

HOW MUCH INSURANCE TO TAKE:

Determining how much life insurance you need is an important decision you should be realistic and consider ALL your present and expected future expenses. After all, this is the only financial security your family will have if you were to pass away unexpectedly.

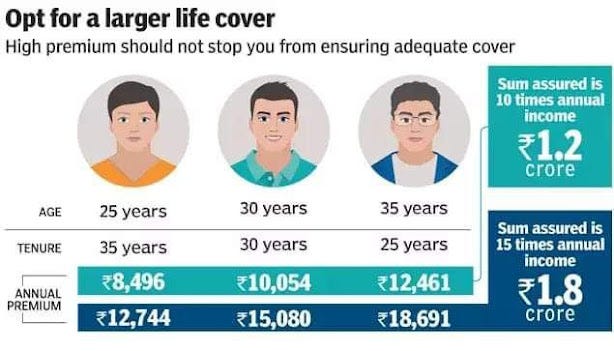

There are many formulas for calculating HOW MUCH Life Insurance is to be taken and the most popular one is to take 10 TIMES OF YOUR ANNUAL INCOME.

But it would be prudent to consider your financial goals like buying a house, provisioning for your needs like children’s education, and of course, making sure that your loans/debts are taken care of.

Your Life Insurance Coverage Amount should cover all the above and a bit more.

By Bit more, I mean to say that you are better off erring on a HIGHER amount rather than lower. It’s better to have more than less!

DON’T FORGET INFLATION:

The Term Insurance claim amount you might need today can be much lower than what you’ll need 30 years from now. Always account for inflation when calculating your life insurance coverage.

Over time, the cost of living rises, eroding the purchasing power of money. To ensure your loved ones are well-protected, it’s crucial to account for this inflationary effect when calculating the coverage amount for your insurance policy.

=======================================

TILL WHAT AGE SHOULD MY LIFE INSURANCE COVER:

Normally, people take Insurance till their retirement age.

A Typical Agent suggests taking Insurance till you are 80.

The decision of whether to take an insurance policy till retirement age or beyond that depends on several factors, including your individual needs and circumstances.

Retirement means Financial Independence. Ideally, when you retire from active earning work, you would have sufficient retirement corpus built up during your earning years, free of all your debts (including home loan), and moreover, your children too would be standing on their feet (earning on their own) and thus you are free from any financial obligation.

REMEMBER, LIFE INSURANCE IS TAKEN NOT FOR YOU TO BECOME RICH

BUT

LIFE INSURANCE IS TAKEN TO MAKE YOUR FAMILY DOES NOT BECOME POOR

REVIEW PERIODICALLY :

Buying life insurance is not a one-time affair.

You should review your life insurance coverage periodically (say once every 5 years) to ensure that it still meets your needs and goals. Life insurance needs can change over time due to changes in income, expenses, and other factors.

Your income may grow, you may make get into more debt obligations, your family size may increase, and even your health could have undergone a change. Even Inflation could have gone up significantly making your dream house that much more expensive resulting in a higher EMI and thus a higher debt obligation.

If necessary, you may need to enhance your insurance coverage amount.

SPECIAL TIP

1. Premium for 60 lacs of term plan in an Insurance company is cheaper than 40 lacs of premium — And this is true for a lot of term plans.

This is because 50+ lacs plans get discounted premiums and medicals are also compulsory.

This is the reason why one should take a term plan for more than 50 lacs even if your initial intent was for a lower sum, as the premium difference is minimal and financially advantageous.

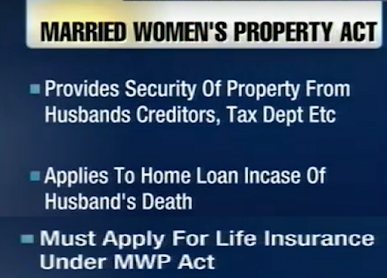

2. Take Insurance under the MWP ACT:

MARRIED WOMEN’S PROPERTY ACT:

Once you have taken Life Insurance Policy, don’t be under the wrong impression, that the entire proceeds of the Insurance policy will go to your wife, If you have any outstanding loans when you die, your life insurance claim money will first be used to pay off those loans. This is because loans are secured debts, which means that they have priority and have to be settled first, and only then the balance is given to your family.

However, there is a solution to this……

if you’re a married male, you can sign the Married Women’s Property Act (MWP) addendum when purchasing term insurance. This ensures that the insurance payout is safeguarded from loans and obligations and is directly provided to your wife. Remember, this option is available only when you initially buy the policy, not afterward.

Hence, while taking a Life Insurance Policy, make sure you sign on the MWP clause and please note this benefit is FREE and doesn’t cost you anything extra.

================

==============================================================

FINALLY,

If you are unsure about how much life insurance you need or what type of policy is right for you, it is a good idea to speak to a financial advisor. They can provide you with personalized guidance based on your individual needs and circumstances. A financial advisor can help you to assess your financial situation, your dependents, and your financial goals. They can then help you to determine the right amount of life insurance coverage for you.

AN EXAMPLE TO HELP YOU UNDERSTAND THE POWER OF WHY LIFE INSURANCE IS REQUIRED

Imagine that your income is a river that flows into a lake.

The lake represents your family’s financial security.

If you were to pass away, the river would stop flowing, and the lake would eventually dry up.

Life insurance is like a dam that keeps the river flowing into the lake, even after you are gone.

The size of the dam (i.e., the amount of life insurance you have) should be big enough to keep the lake full, even if the river flows a little slower (i.e. if your income decreases after you retire).

It is better to have

Life Insurance cover 5 years early. rather than 1 day late!!!

And I end this educative article with this evergreen quote

“ A man who dies without adequate life insurance should come back and see the mess he has created”- Will Rogers

Regards

Srikanth Matrubai